This is part one of a four-part series. Read part two, part three or part four.

Not all private debt is the same – why investors shouldn’t overlook this enticing alternative asset class.

Senior Portfolio Manager, David Saija and Portfolio Manager, Lucie Bielczykova provide insight on the impacts of inflation, rising interest rates and widening credit spreads on Australian and New Zealand private debt as they evaluate the next phase of the economic cycle. Given the timing and shape of the recovery still remains unknown, investors shouldn’t overlook this alternative asset class which can provide much needed capital preservation during these uncertain times.

In the current environment of surging inflation, rising rates, widening credit spreads, and volatile financial markets, there is little doubt that the orchestrated slowdown of developed market economies by Central Banks will cause businesses and consumers to come under increasing pressure. The risk of a global recession is now increasing as a result.

In these periods of challenging economic conditions, the key attributes of Australian and New Zealand private debt have proven to be very attractive and can offer investors a level of protection, namely due to:

1. Floating rate

As base interest rates have risen the yield of the portfolio has risen, thereby insulating performance against inflationary forces;

2. Secured nature of loans

All loans in Revolution’s portfolios are secured (over the underlying assets or assets of the business) which provides strong protection in periods of macroeconomic downturn;

3. Diversification and low correlation

Private debt offers the ability to invest in industries and sectors that are not easily accessed through liquid markets. Moreover, the low correlation to volatile liquid markets and traditional asset classes is also attractive to investors, as private debt provides capital stability in an investor’s portfolio while delivering a steady income stream.

Looking ahead, asset allocators have been asking about the stability of the private debt sector during economic turbulence, the fundamental health of underlying borrowers and the ability of borrowers to continue to service and repay what was taken out as cheap debt.

In the period ahead, the market is now expecting to experience weakening credit fundamentals, particularly interest coverage metrics and serviceability, as well as increasing default rates as borrowers attempt to adapt to the new economic environment.

While it is important to note that we are coming off a relatively benign period where companies are generally in a much better shape compared to the pre-GFC period − with more conservative balance sheets and less leverage in the capital structure, there will be borrowers that can withstand and adapt to the changing environment, and there will be pockets of the market and strategies that will find it increasingly difficult to navigate this period.

As such, it is more important than ever for investors to understand what’s under the hood of their private debt allocation, as there is no doubt the period ahead will see huge dispersion of performance of private debt funds, depending on the focus of the respective strategies and underlying exposures.

Partnering with the right manager – asset selection and credit discipline key to success

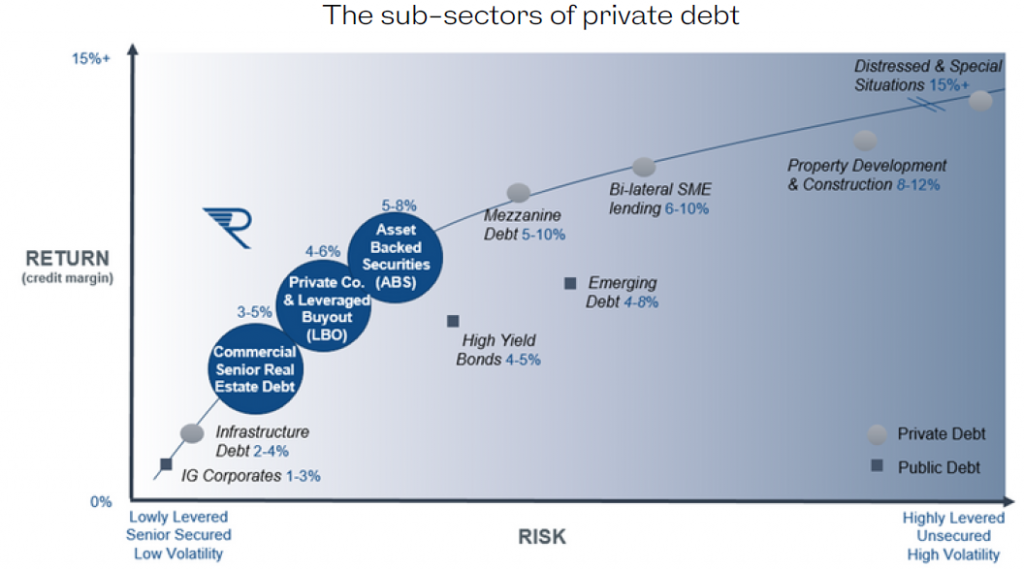

While the investable universe of private debt is broad, Revolution focuses on three key areas being Commercial senior real estate debt, Private company and leveraged buyout debt (LBO) and Asset Backed Securities (ABS). Revolution believes these segments offer the best risk-adjusted returns when compared to other segments in the private debt universe.

Source: Revolution Asset Management

Similar to the broader market, investors have repeatedly asked about the ability of Revolution to be able to navigate through what appears to be a challenging period over the next 12-18 months.

Revolution’s strategy has always been focused on capital preservation throughout economic cycles. As such, focusing on the downside risk for all loans that are advanced is the core of Revolution’s investment process. It has always been an imperative to ensure that there is demonstrated serviceability and repayment of all loans through any macro-economic downturn or recession.

The current state of the portfolio is robust, as a direct result of Revolution’s investment philosophy. Revolution avoids cyclical industries and focuses on those industries that are best able to navigate through a more volatile period – industries such as healthcare, mission critical software and consumer staples. Within those industries, Revolution targets market leading players with strong ability to maintain margins throughout the cycle. Furthermore, ABS are predominantly secured against prime borrowers with higher underlying credit scores, with these borrowers having a much better ability to deal with challenging economic conditions than weaker borrowers.

Whilst the future remains uncertain, the investment team at Revolution has the benefit of receiving very timely private side information on all portfolio loans, to assess how they are performing, coupled with stringent third-party oversight for asset performance and valuations.

All assets are independently reviewed by a specialist valuation firm that utilises all available private side information on a monthly basis to confirm if loans are performing.

Overall, Revolution’s private debt strategy offers many features that are very appealing in the prevailing market for clients as diverse as large superannuation funds, not-for profits and foundations, family offices, endowments and high net worth investors. The combination of capital stability, high income component with low correlation to traditional fixed income and risk assets across a diversified pool of loans is an attractive strategy to minimise interest rate sensitivity and guard against inflation risk as we enter a period of continued market and economic volatility.

Is private debt ready for recession? – a four part series

Missed the previous parts of Is private debt ready for recession? Click the links below to go to:

- Part one – Not all private debt is the same

- Part two – Reaching for resilience as we take a closer look at leveraged loans

- Part three – Considerations when investing in real estate debt

- Part four – A closer look at Asset Backed Securities

For more information on performance and the portfolio of loans or about the Revolution Private Debt strategy, contact us.

This article is for institutional and professional investors only and has been prepared by Revolution Asset Management Pty Ltd ACN 623 140 607 AFSL 507353 (‘Revolution’) who is the appointed investment manager of the Revolution Private Debt Fund I, the Revolution Private Debt Fund II and the Revolution Wholesale Private Debt Fund II (together ‘the Funds’). Channel Investment Management Limited ACN 163 234 240 AFSL 439007 (‘CIML’) is the Trustee and issuer of units for the Funds. Channel Capital Pty Ltd ACN 162 591 568 AR No. 001274413 (‘Channel’) provides investment infrastructure services to Revolution and Channel and is the holding company of CIML. None of CIML, Channel or Revolution, their officers, or employees make any representations or warranties, express or implied as to the accuracy, reliability or completeness of the information, including forecast information, contained in this document and nothing

contained in this document is or shall be relied upon as a promise or representation, whether as to the past or the future. Past performance is not a reliable indication of future performance. All investments contain risk. This information is given in summary form and does not purport to be complete. To the extent that information in this document is considered advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling units in the Funds please note that it does not take into account your particular investment objectives, financial situation or needs. Before acting on any information you should consider the appropriateness of the information having regard to these matters, any relevant offer document and in particular, you should seek independent financial advice. For further information and before investing, please read the relevant Information Memorandum available on request.